First off, this post is about the changes to the PPP program in the Paycheck Protection Program Flexibility Act of 2020 only. If you want a full breakdown of the PPP program please check out other blogs which go into much more detail.

Second, we understand you are frustrated, and the changes are two months late and a dollar short, but there’s still lots of good news and reasons why this may be our most important blog post since the CARES Act was passed over two months ago on March 27th.

The guidance from the SBA interpreting the PPP has been untimely, inconsistent, and incomplete. And many of you have been patiently waiting for these changes and watching as your 8 week period approaches any day, or has possibly even passed. So let’s get right into it so you don’t have to wait any longer.

If you’d rather listen, Eric is explaining his thoughts in a short 8 minute YouTube Video Here:

Want to skip ahead?

- · H.R.7010 Passed by Both Houses and onto President for Signature

- · The Four Horsemen of PPP Forgiveness Reduction

- · New PPP Regulations Change the 75% Rule

- · New PPP Regulations Change the Full Time Equivalent (FTE) Head Count Requirement

- · Remaining PPP Forgiveness Reductions: Reducing Pay

- · Remaining PPP Forgiveness Reductions: EIDL Funds

- · But Wait There’s More! Improved Repayment Terms

- · Updated PPP Forgiveness Application

- · The US Treasury Can Still Screw It Up

- · Ask us YOUR question!

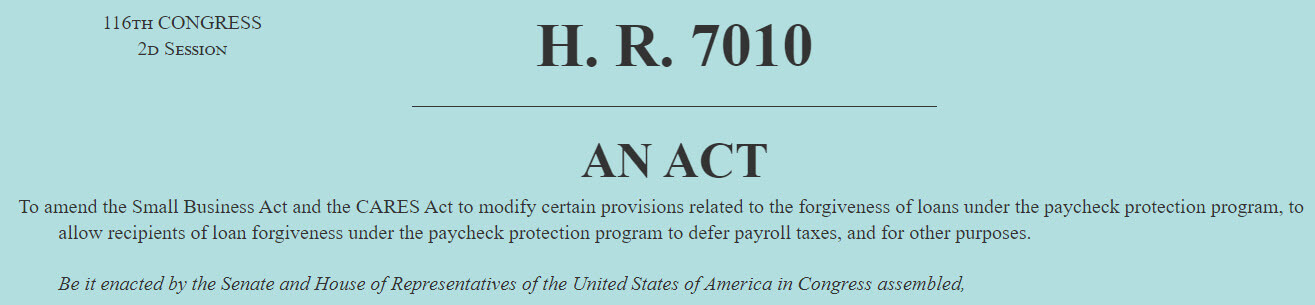

H.R.7010 Passed by Both Houses and onto President for Signature

Today, June 3, 2020 the Senate passed the H.R. 7010 bill that Congress wrote and passed last week. With both houses in unanimous agreement, the president is expected to sign in a day or two. This has been the long-awaited patch to the PPP program business owners, CPAs, bankers, and even members of congress have been clamoring for. The bill itself is a short one page document that changes key terms and definitions in the Cares Act law.

There are some good things here and some big glaring oversights but we’ll get into that in a minute.

The Four Horsemen of PPP Forgiveness Reduction

First, understand the PPP program allows for forgiveness of the loan amount provided certain criteria are met. This is the carrot everyone has been chasing for two months: what do I have to do to get my loan forgiven (also known as: how do I get my free money)?

Prior to today, there were generally four ways to have your PPP forgiveness reduced or limited and they are:

- · Using less than 75% of the funds for payroll within 8 weeks

- · Reducing your headcount or Full Time Equivalent (FTE)

- · Receiving EIDL funds.

- · Reducing a single persons pay below 75% of the lookback period

This is an overly simplistic summary, but works to illustrate the limitations most fitness business owners are facing and how H.R. 7010 helps loosen these restrictions.

New PPP Regulations Change the 75% Rule

The two major changes to the bill are that:

- · Only 60% of the funds are required to be used for payroll (rather than 75%) and…

- · Business owners have 24 weeks rather than 8 weeks.

This is a major reprieve for gyms and fitness studios across the nation who have been wondering: how do I meet the 75% requirement when my facility is closed and my employees are home? If you’ve been reading our content or attending our webinars, we’ve been counseling everyone to only pay workers who are currently working because we predicted, correctly, that these changes were coming. It’s unfortunate for owners who did not have professional advice (or the right professional advice) and ended up paying workers who were staying at home, but here we are. Let’s focus on the road ahead. Need a CPA who is in your corner next time you need to make a complicated decision? Let us know how we can help by getting in touch here.

This 24-week period should make it fairly easy for owners of almost every kind to meet the 60% threshold and is the only piece of good news I have received so far this year. 2020… I’m looking at you!

If you’re still having trouble, remember that the 24-week period begins either on the date you received the funds, or you can choose an alternative period and start your 24 weeks on the pay date after you receive your funds, possibly providing you with an additional two weeks.

And if you’re still having trouble, here are other strategies we can advise on:

- · Hire back more help

- · Pay existing team more (bonus or hazard pay)

- · Convert independent contractors as employees

- · Contribute to retirement plan / health insurance

- · Hire non-shareholder family (pending guidance from the US Treasury)

- · Paying back the funds

New PPP Regulations Change the Full Time Equivalent (FTE) Head Count Requirement

Originally the law reduced your PPP forgiveness by the percentage of employees that weren’t brought back by June 30th. And sure, you could bring back people to replace employees who weren’t coming back but many businesses are not what they once were and either can’t or don’t have the capacity to have the same level of staffing. COVID19 gutted businesses more than Congress anticipated back in mid-March when the Cares Act was written.

Fix #1: The Flexibility Act extends that time to December 31, 2020.

Fix #2 H.R. 7010 renders the headcount requirement largely a non-issue. It does this by providing an exemption of sort to businesses that certify in good faith that they are:

- · unable to rehire former employees and is unable to hire similarly qualified employees; and

- · unable to return to the same level of business activity due to compliance with government requirements or guidance related to COVID-19.

- The details say if the business “is able to document an inability to return to the same level of business activity as such business was operating at before February 15, 2020, due to compliance with requirements established or guidance issued by the Secretary of Health and Human Services, the Director of the Centers for Disease Control and Prevention, or the Occupational Safety and Health Administration during the period beginning on March 1, 2020, and ending December 31, 2020, related to the maintenance of standards for sanitation, social distancing, or any other worker or customer safety requirement related to COVID–19.”

This seems like a nice low bar for most fitness business owners. With this exemption, almost every business in America that has been affected by COVID19 shutdowns and closures should be relieved of meeting the FTE requirement. In the odd business that is doing better, chances are that you’ve had to staff up to support your growth.

Also good news, this was perhaps the most complicated part of the forgiveness calculations that had accountants reeling over the amount of work involved to project and plan for how much of the PPP funds would need to be paid back. It’s unclear whether we need to still math out the full-time equivalent differences on the forgiveness application at all. I’m hoping the forgiveness application is simplified.

Remaining PPP Forgiveness Reductions: Reducing Pay

The Paycheck Protection Program Flexibility Act is silent on the 3rd potential reduction in PPP forgiveness. So unless something changes, you’ll need to pay at or greater than 75% of their previous pay. This goes for both salaries and for hourly rates.

If you need to keep pay reduced, as long as you bring it back to normal pay rates by the earlier of December 31, 2020 or the date your file your PPP forgiveness application you are okay. Otherwise, you may need to pay back a portion of your PPP funds.

Our recommendation is to bring pay levels back to where they were previously by the dates specified.

Remaining PPP Forgiveness Reductions: EIDL Funds

The Paycheck Protection Program Flexibility Act is also silent on the 4th potential reduction in PPP forgiveness. So unless something changes, your PPP forgiveness is reduced by the amount of the EIDL Grant you may have received ($1,000 per employee up to $10,000 maximum). We never expected changes to this portion of the law as the intent is to keep business owners hands out of both cookie jars.

But Wait There’s More! Improved Repayment Terms

The Paycheck Protection Program Flexibility Act improves the repayment terms from two to five years and includes a 10 month deferment period. So if you have had your forgiveness reduced for any reason, those funds are paid back over 5 years at a rather generous 1% interest rate. The Flexibility Act also allows for PPP loan recipients to defer payroll taxes where previously they were ineligible. We don’t recommend any business owner get behind on payroll taxes and do not recommend utilizing this strategy.

Still Unclear and Forever Waiting

Several items remain unclear:

- · Do schedule C filers PPP loans get automatically forgiven since they have no employees? We think so.

- · Do wages paid to family members of shareholders or owners of the business count towards the 60% requirement? The US Treasury has not released guidance on this 10 weeks after the CARES Act was passed (as of this writing).

- · Will the $15,385 limit on employee and owner compensation includable in the forgiveness calculation increase?

- · Expenses paid for with PPP funds are still not deductible according to the US Treasury contrary to the CARES Act itself. We expect this to be litigated in courts if it is not fixed soon by congress.

- · There are still dozens of unanswered questions we expect to be released to address a myriad of other nuanced issues now that the Flexibility Act has been passed.

Rubber Stamp Glimmer of Hope is Fading

Our hope was that loans under a certain dollar amount would be completely forgiven. Say, for example, loans under $150,000 or $500,000 would not need to meet any requirements at all. This seemed to make sense to the CPAs and bankers across the nation that we spoke with. For a while, it seemed like this rumor floating around was a real possibility. Now with the passage of the Paycheck Protection Program Flexibility Act of 2020, I believe the chances of “rubber stamping” loans of any amount are much less of a reality.

Updated PPP Forgiveness Application

As a small business owner and CPA I was hoping for the Rubber Stamp that would eliminate the need for the forgiveness application entirely. And while the Paycheck Protection Program Flexibility Act of 2020 greatly helps most business owners qualify for maximum loan forgiveness, it still burdens business owners, accountants and bankers with the forgiveness application process. Let me tell you: these 11 pages are not fun. And while better now than before, I am anxiously awaiting to see if the US Treasury blesses us with a simplified and streamlined forgiveness form.

The US Treasury Can Still Screw It Up

It’s important to note that the US Treasury interprets the financial and tax laws. And while the Paycheck Protection Program Flexibility Act of 2020 seems incredibly clear on its intentions, the US Treasury has already directly contradicted the CARES Act numerous times. So we’ll wait with bated breath to see what the US Treasury does with this simple one page change. Tony Nitti summed it up best by saying: “I’m not sure what type of wiggle room they’ll have given the statutory language, but when you consider that the SBA pretty much took a blowtorch to the legislative text of the CARES Act, I guess anything is possible.”

Have a Question About The Paycheck Protection Program Flexibility Act? We Have Your Answer

This Paycheck Protection Program Flexibility Act 2020 should hopefully clarify many of your questions, but we know this is confusing stuff. If you have a question, even if you’re not our client, you can ask us a question related to your specific business below.

In the meantime, check out our COVID-19 Resource Hub where we’ve compiled our latest blog posts & YouTube videos along with third-party resources that we find valuable. There is some great stuff in there.

Have A Specific Question About PPP?