Follow us on YouTube and click to watch Eric discuss the topic here!

The original title of this article was “Which Government CARES Act Pays You The Most? With Downloadable Decision Matrix” but I think we did a much better job with the ode to the woman, the myth, the legend, Oprah herself – what do you think?

Welcome back to The Fitness CPA’s Covid-19 series. If you missed last week’s video and/or blog, you can check out how to work with your landlord on this and next month’s rent while you’re closed, here.

This week, we’re providing an overview of the options available to gym and fitness business owners under the Coronavirus Aid, Relief, and Economic Security (CARES) Act. Our goal is to lay out the options available to business owners who have been adversely affected by COVID-19. That’s you…. so check out the rest of this post and work with your advisor to decide which option is best for you and your business.

This post isn’t meant to get into the nitty gritty details. If you want that, we’ve provided links to better resources. Think of it as the “lay of the land” with practical advice for why you might want one option over another.

Already done your research? Just need to know the practical how-to? Skip ahead to a Practical Strategy and Application of the Cares Act in 6 Easy Steps. You won’t find this anywhere else. After two days of exhaustive research, this is our original 6-step solution to the 800+ page CARES Act for small business owners.

Still have questions?

We did an 18 question Government Bailout, PPP and EIDL Q&A here in this blog post.

And we did a special Paycheck Protection Program Q&A here in this blog post here.

And many of the answers can be found here in this senate guide Q&A.

TIP: If it’s not clear whether the ERTC or PPP is best for your business, we recommend running numbers to make that determination. We hope to provide templates to make that comparison in the coming days.

Skip ahead to:

- What is the CARES Act… and More Importantly, Why Should You Care?

- Save Thousands… But Act Now! Funds Are Only Available for a Limited Time!

- Debt Relief on Existing Small Business SBA Loans

- Delay of Employer Payroll Taxes

- Employee Retention Tax Credit (ERTC)

- Paycheck Protection Program (PPP)

- Paycheck Protection Program (PPP) Loan Forgiveness

- SBA Economic Injury Disaster Loan (EIDL)

- Practical Strategy and Application of the Cares Act in 6 Easy Steps

- Just Tell Me, How Do I Get My Free Car… errrr… Bailout?

- Download The Decision Matrix and Loan Application Preparation Form

- Will The Fitness CPA Help Me With What’s Next?

What is the CARES Act… and More Importantly, Why Should You Care?

On Friday, March 27th the United States government passed a $2.2 Trillion dollar stimulus package to help those affected by COVID-19. It was written to help businesses like yours (and individuals) who have been shuttered during the coronavirus outbreak. There are several programs available that may help you and your business survive and thrive after COVID-19 is history. In order to participate in the program and obtain economic relief, you need to take certain actions such as:

- · Prepare for the loan application

- · Decide which program is most beneficial

- · Ensure your business qualifies for the desired program(s)

- · Apply <— the most important part. Don’t forget to apply.

- · Obtain funds and use them in your business.

- · Pay back the funds, or apply for loan forgiveness in the case of one program.

Save Thousands… But Act Now! Funds Are Only Available for a Limited Time!

No this isn’t a 3:00am infomercial. Funds really are limited and preparing for your application now may be the difference between obtaining thousands of dollars of stimulus money for your business, or nothing at all and closing your doors.

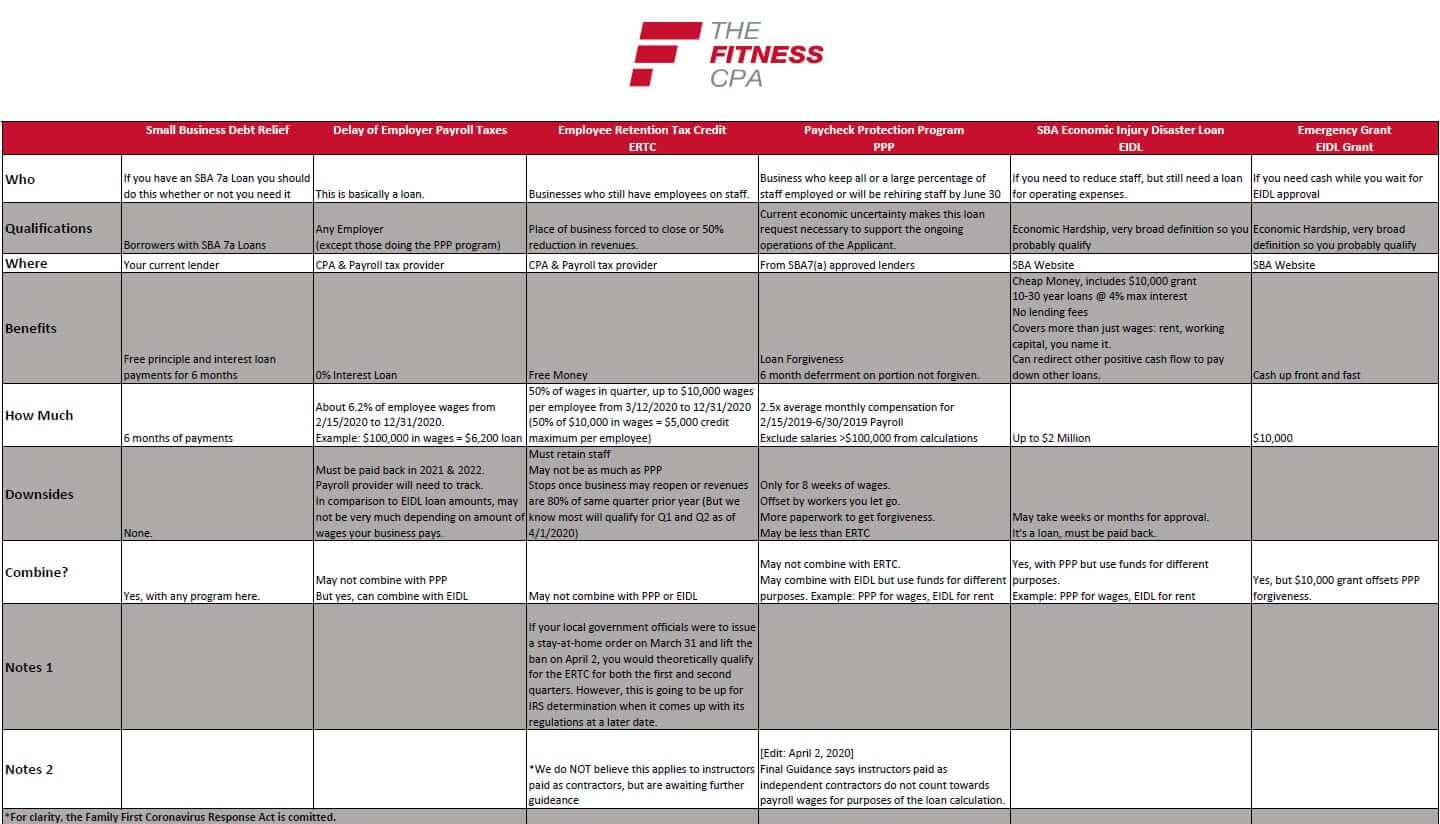

In the video above we go into detail about the options available to fitness business owners under the Coronavirus Aid, Relief, and Economic Security (CARES) Act including:

- · Small Business Debt Relief

- · Delay of Employer Payroll Taxes

- · Employee Retention Tax Credit (ERTC)

- · Payment Protection Program (PPP)

- · SBA Economic Injury Disaster Loan (EIDL)

- · Emergency Grant

Sure we wrote about it here, but the video and the downloadable guide are a better bang for your buck. If you insist… keep reading below.

TIP: We recommend focusing on the “Who” line on the Matrix as this may help steer you in a more clear direction.

Debt Relief on Existing Small Business SBA Loans

If you have a SBA Loan there is absolutely no reason not to take advantage of this program. In fact, it should be automatic. But call me crazy, I don’t trust the government or lenders very much.

ACTION: Contact your lender to ensure your loan is placed on the six-month debt relief program.

The stimulus package Congress recently passed ensures every small business with a loan from the Small Business Administration (SBA) will be relieved of their loan payments for the next six months. The SBA will make payments on behalf of small business borrowers to cover 6 months of payments. This provision would relieve small businesses of their loan payments entirely, including principal, interest, and fees.[Edit] Guidance has told us that the six months should be automatic. But we recommend checking with your lender to ensure.

How will this interact with the new Paycheck Protection Program loan described below?

- · While SBA borrowers are receiving the six months of debt relief, they may apply for a Paycheck Protection Program (PPP) loan that provides capital to keep their employees on the job.

- · The six months of SBA payment relief may not be applied to payments on PPP loans. However, those loans already have forgiveness provisions that essentially make them grants if you meet certain requirements. (See below for more information!)

Delay of Employer Payroll Taxes

This is basically a small loan, equal to 6.2% of wages your business pays to employees between now and December 31, 2020.

Pairs well with the ERTC but initially might not amount to much if employer taxes are offset by ERTC credits.

Also pairs well with EIDL Loans below.

- · Loan means this must be paid back. At 0% interest it’s not a bad deal, but for many gyms this won’t amount to much, perhaps $3,500-$15,000.

- · 50% of the loan is paid back in 2021, and the other 50% is paid back in 2022.

- · It’s either this program or the Paycheck Protection Program. You can’t do both.

Employee Retention Tax Credit (ERTC)

This works better if you have staff still on payroll. So if this isn’t you, see ya! Skip on to the next one.

Pairs well with the Delay of Employer Payroll Taxes (above).

Your business qualifies for ERTC if your business:

- · lost 50% or more of your revenues but unless you decided to stop charging all members, this probably isn’t you.

- · was forced to close by a 3rd party including the government (federal, state, county, or city) or even your franchisee or landlord.

If you want to nerd out, you should check out Markowitz Accounting Blog: Employee Retention Tax Credit here.

But basically:

- · This could be free money to you, which could amount to thousands of dollars that don’t need to be paid back. That’s how “credits” work.

- · How much? 50% of wages in the quarter, up to $10,000 wages per employee from 3/12/2020 to 12/31/2020 (50% of $10,000 in wages = $5,000 credit maximum per employee)

- · Stops once the business reopens its physical location (you may still operate virtually or from temporary / at home locations)

- · Cannot combine this with Paycheck Protection Program (PPP) or Economic Injury Disaster Loan (EIDL) listed below.

- · Don’t overlook this ERTC program, it may be more valuable than the more notable PPP program listed next.

- · Full FAQ from the IRS is here: https://www.irs.gov/newsroom/faqs-employee-retention-credit-under-the-cares-act

TIP: Run or hire your accountant run the numbers on ERTC vs PPP to figure out which is best.

Paycheck Protection Program (PPP)

Final guidance on the Paycheck Protection Program is here at this link (released April 2, 2020)

This is the program that’s all over the news. The PDF of the application was released today, March 31st, 2020. I heard from one credible source the application will go live on Friday, April 3rd. Do you want to be the first in line? Let’s see.

- · This program is for:

- · Businesses who keep all or a large percentage of staff employed or will be rehiring staff by June 30

- · Businesses whose “Current economic uncertainty makes this loan request necessary to support the ongoing operations of the Applicant.” Yes, that’s you – without question. It’s a low bar to qualify.

So what’s the big deal?

Paycheck Protection Program (PPP) Loan Forgiveness

Ah, there it is. It practically says free money in the name. Loan forgiveness means the SBA (Small Business Administration) will loan you the money and your business won’t need to pay it back.

“Really? Are you sure? I know things are bad, but I’m going to get free bailout money to wipe my tears?”

- · Like all things, it comes with a set of criteria. But if you keep most of your employees working you could stand to benefit by several thousand dollars.

So, why not do this?

- · If you don’t keep most of your workers employed, you may be responsible for paying back a portion of this loan. A loan? Gross! I know what you’re thinking “wait, I thought you said this was free money?” There’s always a catch.

- · The Employee Retention Tax Credit may be worth more. But you have to do the math.

- · There’s a bunch of paperwork to get loan forgiveness. Nothing really is free, is it?

- · This money is only worth 2.5 months worth of your payroll costs and after that, you’re on your own again. Fortunately, you can combine this program with the Disaster Loans program. That’ll be just a little bit later here…

TIP: On the application itself available at this hotlink, you’ll want to check that the money is for payroll, rent, and utilities. We recommend checking all three boxes except not the “other” box. Also, be sure to include your contract workers in the number of jobs. I wouldn’t worry about being too exact on this right now, as it will be much more detailed on the forgiveness application. But you should fill the application out to the best of your ability.

If you want to nerd out and learn things – like salaries over $100,000 don’t count and step-by-step calculations – you should check out Markowitz Accounting Blog: Payroll Protection Program

For basic resources from the US Treasury that provide an overview of the program, click here:

- For a top-line overview of the program click here.

- Borrowers, for more information click here.

- The application for borrowers can be found here.

Want help on deciding PPP vs ERTC? Oh yes, you do. And you can find that comparison here.

TIP: Instructors paid as contractors do count towards the calculations. The US Treasury could always come out with a technical correction, but because the gig economy is so big now contractors are included the way the law is written.

We’ve just released a PPP Q&A Blog – check it out here.

SBA Economic Injury Disaster Loan (EIDL)

These EIDL loans have been around for a while and were used most notably after Harvey and Katrina. Just as the name implies, it’s a loan that needs to be paid back. But it’s a pretty good deal:

- · Very broad definition of economic hardship so yes, your business qualifies.

- · $1,000 per employee up to $10,000 will be paid directly to you, upfront, within 3 days [despite the 3-day listed timeframe it’s been more like 2-4 weeks for most to receive this so far], but then the rest of money could take weeks or even months to arrive. The $10,000 is supposed to help bridge that gap.

- · At 3.75% interest and terms of 10 to 30 years it’s cheap money by any standard.

- · There are no lending fees.

- · Funds can be used for (almost) anything including rent, payroll, utilities, overhead expenses and other working capital items.

- · We had heard these funds may be capped at $25,000 per loan but nothing official has been announced and we’ve seen much larger amounts arrive in clients accounts but thought we should mention this potential $25,000 cap.

This can be used in combination with the PPP loan above.

Practical Strategy and Application of the Cares Act in 6 Easy Steps

The programs only work together a few ways so you’re going to do this:

- Small Business Debt Relief if you have an SBA Loan

- Either

- · Employee Retention Tax Credit

- or

- · Paycheck Protection Program (PPP)

- · Employee Retention Tax Credit

- If you chose ERTC

- · Add Employer Payroll Tax Delay if you need additional help. But initially might not amount to much if employer taxes being offset by ERTC credits.

- If you chose PPP

- · Add on Economic Injury Disaster Loan

- · Don’t forget to get that sweet $1,000 per employee up to a maximum of $10,000 grant money, but be aware it will offset the PPP loan forgiveness if you got the PPP loan.

- If no employees, then ERTC and PPP aren’t available or if they are valued at less than the potential for $10,000 EIDL try EIDL.

- If you happen to have applied for a disaster loan already either:

- · Pursue the PPP if you still have employees if the projected value is >$10,000 or

- · Request the $10,000 grant money.

Now, of course, it’s much more complicated than that. But that’s the only way the program can be combined so within those confines you will find the best answer for your business.

Just Tell Me, How Do I Get My Free Car… errrr… Bailout?

Download our decision matrix here. Seriously, it’s free and it will help a lot. I actually don’t even know why I wrote this blog, it’s all in the chart and video which is a lot easier to digest so go get that.

Then fill out one of the appropriate applications and wait for that sweet stimulus money.

Action: If your business can utilize the Payment Protection Program which has loan forgiveness you must be ready to file that application as soon as this Friday when thousands and thousands of businses owners will be vying for the pool of $350 Billion (with a B).

Still have questions? Most of the answers can be found here in this senate guide Q&A. Or you can messsage me here and I’ll find you the answer.

Will The Fitness CPA Help Me With What’s Next?

We hope you’re getting value out of this COVID-19 series and we’ll continue to update you with new information as quickly as we can.

Remember, it’s likely to be a long road ahead even for the best positioned gyms, boxes, studios or fitness centers. Any relief you can get now from the government the better off you’ll be down the road. The CARES Act was created for businesses like yours and mine – take advantage of the options.

If you have any questions at all, please reach out to my team here or shoot us a comment over on our YouTube Channel. Either way, we’ll respond personally within one business day to help you get the assistance you need.

Follow our emails and YouTube channel in the next coming days and please share with any other business owner who might find this helpful.

We’re here for you, and will continue to do our best to keep you informed over the next coming weeks.