Bailout Money Q&A for the Paycheck Protection Program

We also did a second round of 18 Q&A’s you can read here: Government Bailouts, PPP & EIDL Q&A #2

Yes, that’s the famous J.G. Wentworth Commercial “it’s my money, and I need it now!” It couldn’t be more appropriate.

A lot of questions have come in about the government bailout program called the Paycheck Protection Program. First, be aware the application process opens up Friday, April 3rd and funds are limited. Missed our blog and need to learn more about the program? Check out our last blog post.

Let’s get right to it.

Q: Why are you doing this? Don’t you have family, work and tax returns to tend to?

A: Look, the fitness industry is really fucking hard. But I don’t need to tell you that, right? We’re all in this together. It’s time to share, to help, and lift each other up. That’s what the fitness community is supposed to be about so let’s do that. Please pay it forward.

Q: Should I apply for the Payment Protection Program? Do I need to apply? What if I find out another program is better for me?

A: It’s possible other programs such as the ERTC or EIDL (+ Grant) program (mentioned in my last blog post here) may be more beneficial for you, but given the short timeline we’re recommending all clients apply for the PPP and then deny it if subsequent calculations prove ERTC is better. Think of this as a Black Friday sale potentially worth tens of thousands of dollars to your business. Get in line early – it’s more than worth it.

Q: What exactly do I need to do to get my money?

A: You should apply online through any existing SBA 7(a) lender or through any federally insured depository institution, federally insured credit union, and Farm Credit System institution that is participating. Other regulated lenders will be available to make these loans once they are approved and enrolled in the program. You should consult with your local lending company as to whether or not it’s participating. All loans will have the same terms regardless of the lender or borrower. A list of participating lenders, as well as additional information and full terms, can be found at www.sba.gov.

Q: In English please? Where do I go to get some of that sweet cash? I tried to get an appointment at a bank and could not get one.

A: All applications are online. There is no one to meet with. No bank to go to. Banks who already offer SBA loans will offer these. But many banks are limiting applications to their current customers only. We received an email from three such lenders stating only clients who had been members since Feb 15th were eligible, through their online login, to complete the application with them. You will urgently want to locate the bank or banks you will attempt to apply through.

Q: How do I find these banks?

A: You need to find a bank that will let you apply with them. Some banks are only permitting current customers to apply through them. I would check with:

- · Your current or previous SBA lender

- · Current business checking account bank

- · Current business credit card company

- · Current personal checking account bank

- · Current personal credit card company

Q: Do I really need to get up at 6am ET (4am MT)?

A: I will be up at 6am ET and checking every 15 minutes but I’m also normally up at this hour. We are advising clients to start checking at 6am Eastern Time and regularly thereafter. A lender I trust told me, “This is a good strategy.” Better safe than sorry. Would you get up at this time for several thousand dollars? I would. You’ve got nothing to lose… except sleep.

Q: No seriously, getting up at 6am ET and then… do what?

A: Get online and check their website and keep checking back every 15 minutes until you complete the application. You can also ask your SBA lender when their website will go live.

Q: Will they push the launch date back?

A: As of 5:00am ET on Thursday, no. But it’s entirely possible. If it’s pushed back we’ll post it on social – you’re following us on Facebook, Instagram and Twitter already – right?

Q: Is this really free money that I don’t have to pay back?

A: In many instances, yes. See the blog post for more info. This Q&A is more for the application coming up Friday.

Q: Will the loans really run out?

A: Yes. Only $349 Billion has been allocated. As it stands now, once they are gone, they are gone.

Q: Can you help me complete the application?

A: We are not able to complete the application on your behalf. It is your responsibility to complete the application timely. We are expecting bank websites to crash, have wait times, and generally be a pain to access. Stay strong, be persistent. You do not want to miss out on these funds. It could also be super smooth and a 5-minute process. The SBA application itself is very straight forward.

Q: Do I need to complete the PDF Application you linked to in your blog (also here)?

A: No, but you should know the answer to every PDF question so you don’t get stuck on the application process. The lender may ask for more than what is on the PDF, including things like tax returns, bank statements, payroll reports and drivers licenses of every owner. Have it all ready.

Q: If I get these funds, do I have to pay them back if I permanently close or file for bankruptcy?

A: Great question, that’s currently unclear. I suggest obtaining the money if you need it or declining the loan once approved. We’ll certainly have more guidance on this later.

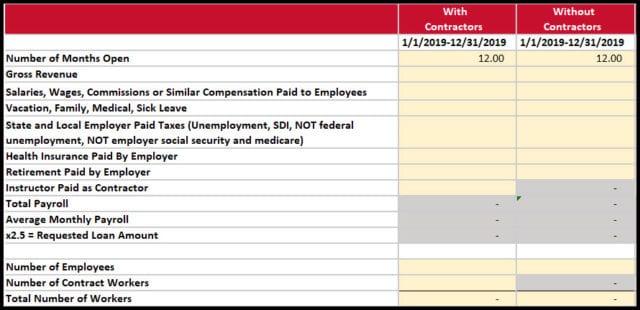

Q: Do independent contractors count towards the payroll calculation?

A: [Edit April 2, 2020] We regret to announce that independent contractors are NOT part of the calculation in the interim rules. It is very clear contractors are mean to be excluded as of 4/2/2020 guidance. The treasury may determine otherwise at a later time but we are advising to include contractor pay in your calculations for average monthly payroll.

Q: How do I calculate the amount of the loan I should apply for?

A: Here’s a link on that: https://www.uschamber.com/report/covid-19-emergency-loans-small-business-guide

A: We also did our own guide here:

Q: I need the larger disaster loan, should I apply for that now?

A: We are advising clients to apply for the PPP program Friday. Then the disaster loans later. Do not apply for the disaster loan (also called EIDL) until you are approved for the Paycheck Protection Program. If in doubt, talk to your Fitness CPA and your lender as there’s a lot of misinformation out there.

Q: If I get an EIDL and/or an Emergency Economic Injury Grant, can I get a PPP loan?

A: Whether you’ve already received an EIDL unrelated to COVID-19 or you receive a COVID-19 related EIDL and/or Emergency Grant between January 31, 2020 and June 30, 2020, you may also apply for a PPP loan. If you ultimately receive a PPP loan or refinance an EIDL into a PPP loan, any advance amount received under the Emergency Economic Injury Grant Program would be subtracted from the amount forgiven in the PPP. However, you cannot use your EIDL for the same purpose as your PPP loan. For example, if you use your EIDL to cover payroll for certain workers in April, you cannot use PPP for payroll for those same workers in April, although you could use it for payroll in March or for different workers in April.

From US Senate: https://www.sbc.senate.gov/public/index.cfm/guide-to-the-cares-act

Actual PDF: https://www.sbc.senate.gov/public/index.cfm?a=Files.Serve&File_id=29FC1AE7-879A-4DE0-97D5-AB0A0CB558C8

Q: My business has not opened yet, am I eligible for the Payment Protection Program?

A: Maybe. Sorry, I know this is not the best answer. We are awaiting guidance as there are several ways to define “open”. I would recommend applying and sorting it out later. Email me [email protected] to run your specific situation by me.

Q: When do I get the money?

A: Unclear at this time. I’m estimating somewhere between 3 weeks and 3 months. But probably 3-6 weeks and the Treasury is currently saying even sooner than this. I’ll believe it when I see it.

Q: I have more questions not listed here or in your blog, who can help me?

A: We can. Email me, [email protected]

Q: But aren’t you going to charge me a lot of money.

A: No, it’s completely free. We’re not charging for our advisory services during this time. If you’re getting value out of our content we’d love if you would like us on Facebook, subscribe to our YouTube Channel and when things improve and you need accounting or advisory help – give us a ring to help you.

Q: How can you afford to give away your advice for free?

A: That sweet, sweet bailout money of course! Just kidding. It’s tough times in the fitness industry and we just want to help. Sure we do the bookkeeping and tax work, but we thrive on the advisory level services. Advisory work means helping you run your business better and more profitably.

Q: You seem really nice! Thanks for the help.

A: That’s not a question, but you’re welcome. Messages like this help fuel me to keep delivering valuable content.

You can sign up for future updates here.